How states can stop EBT theft before it happens: The case for real-time transaction blocking

Our editorial promise

All of our Propel editorial content meets our high bar for accuracy, timeliness, trust, and relevance. Our pages are edited and fact-checked to make sure we meet our mission of giving you information you can rely on.

Learn more about our editorial standards.Every month, millions of Americans rely on their Electronic Benefits Transfer (EBT) cards to put food on the table. SNAP and TANF benefits are a lifeline for households navigating poverty and economic insecurity. And every month, organized gangs of criminals steal those benefits right out of their accounts. State agencies are on the front line of this problem. Every stolen dollar is a crime with many victims: the intended recipient, the caseworker who hears their call, the retailer losing out on sales, the program administrator struggling to manage an influx of complaints, and the taxpayer, whose investment has been wasted.

In 2025 alone, an estimated $600 million in EBT benefits were stolen from families nationwide. That’s $600 million in taxpayer dollars diverted from children, seniors, and families in need, and into the hands of criminals.

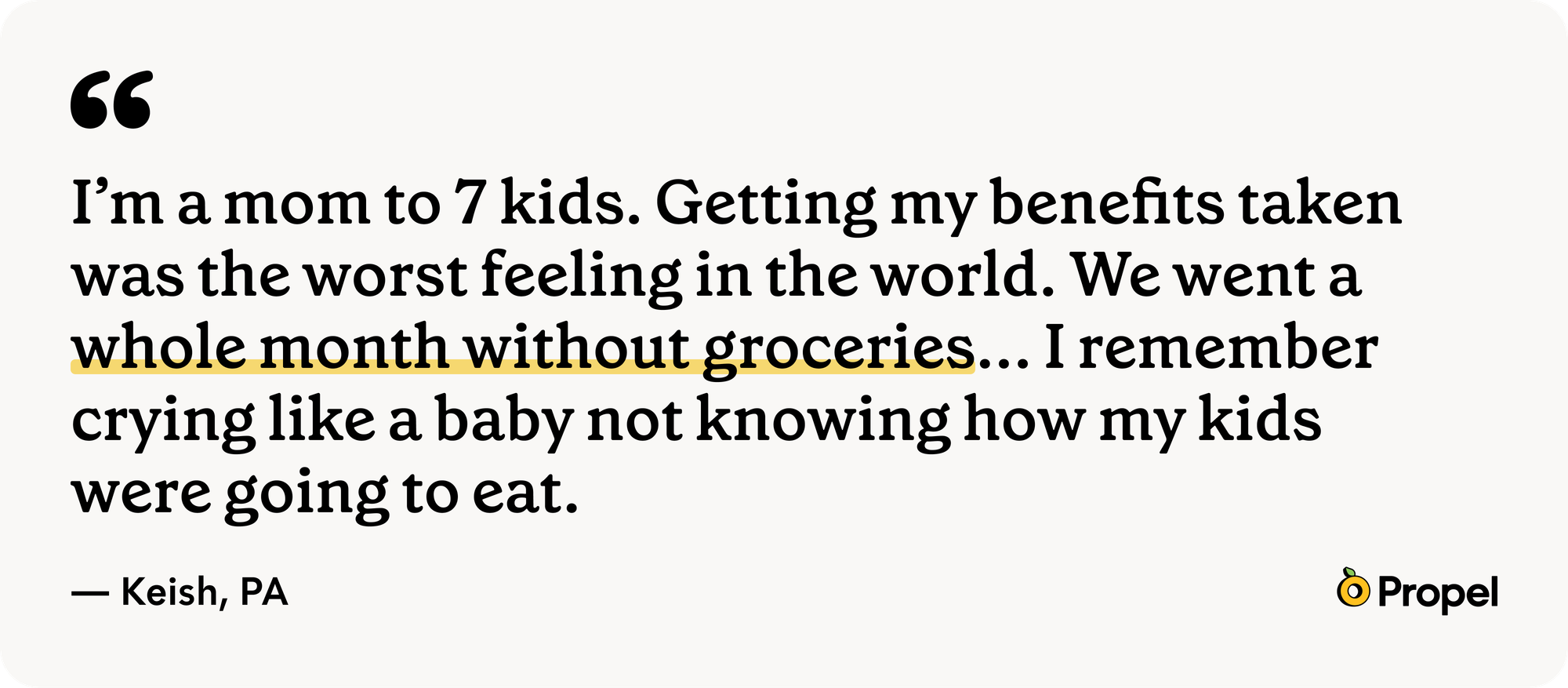

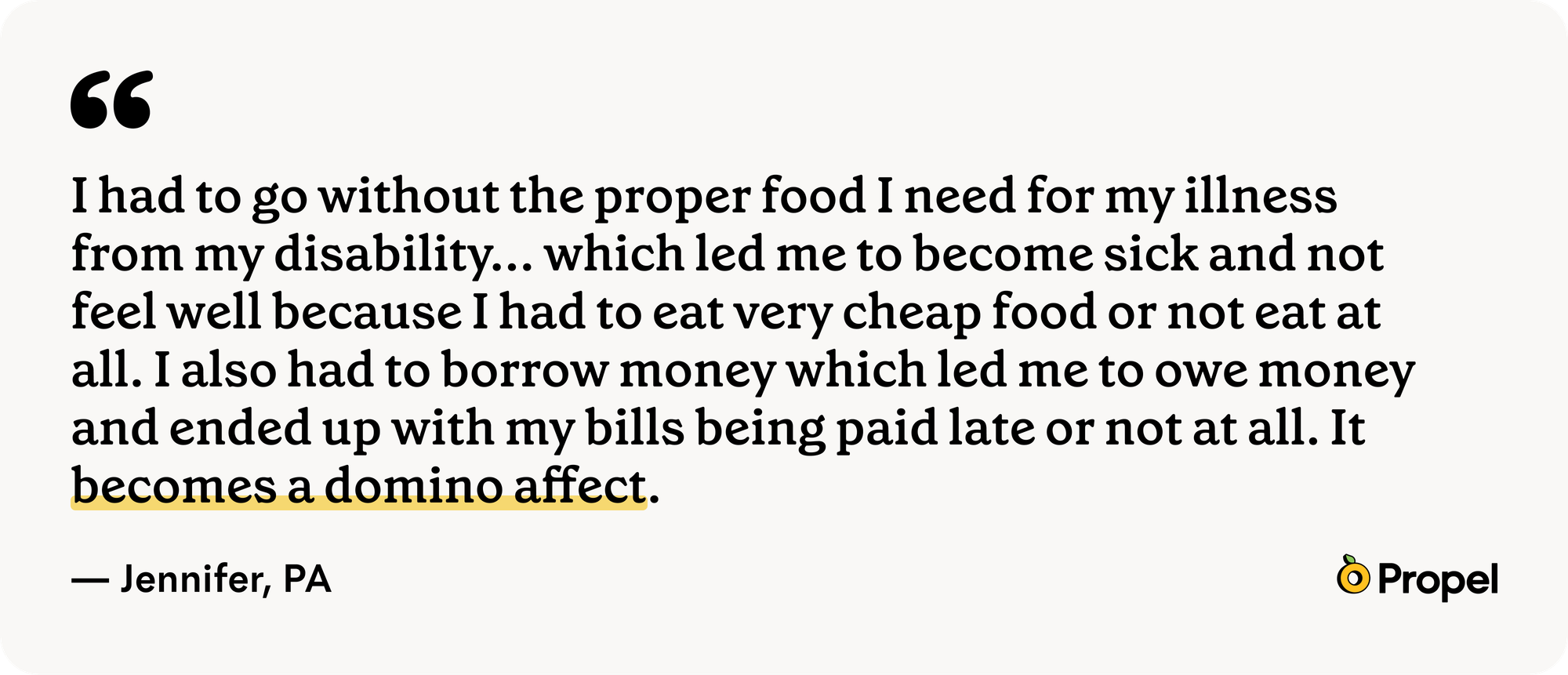

The human cost is staggering. Among recent theft victims surveyed, 56% skipped or reduced meals. 43% borrowed money or went into debt. 35% fell behind on rent or bills.

EBT theft is overwhelmingly perpetrated through card skimming, where criminals install hidden devices on card readers to capture card numbers and PINs. Because the vast majority of EBT cards still rely on magnetic strips rather than the chip technology standard on commercial debit and credit cards, they are uniquely vulnerable. Once card information is stolen, cloned cards are used to drain accounts, frequently on deposit day, which maximizes the criminal’s gain and the damage done to recipient households.

In Propel’s 2026 annual survey of EBT theft, 60% of EBT cardholders said they would feel reassured by automatic 24/7 fraud monitoring that blocks suspicious transactions. More than half said they want chip cards. Families are telling us they want systemic protections with tools that work automatically, in the background, without requiring them to remember to lock their card every time they’re done shopping.

There is no silver bullet, we need layers#there-is-no-silver-bullet-we-need-layers

States have invested meaningfully in fighting EBT theft. Card locking allows households to freeze their cards when they’re not actively shopping. Out-of-state transaction blocking prevents card information from being liquidated across state lines. Chip cards make skimming significantly harder by replacing magnetic strips with encrypted chip technology.

Each of these tools has real value. But each one also has real limitations.

Card locking does not prevent skimming, and requires constant vigilance from the cardholder. Every time they need to buy groceries, they must unlock their card and in that window, they’re exposed. Similarly, Propel users have described barriers to card locking like having limited internet connectivity inside the grocery store, making it difficult to unlock their EBT card in the checkout line. Out-of-state blocking helps with cross-border theft, but criminal gangs are dynamic and adaptive, and often perpetrate theft without regard to their physical location. Chip cards are a powerful systemic protection, but success hinges upon retailer and cardholder adoption. Many consumers still rely on swiping the magnetic stripe due to lack of a chip accepting terminal, damage to that terminal, or other reasons. Chip cards are being introduced slowly, on a state by state basis. This technology is powerful and reduces theft substantially, but they are not a silver bullet, and criminal networks may simply shift their operations to states that haven’t yet adopted them.

We can learn from the private financial services sector–No single tool can stop a sophisticated, adaptive adversary. What works is the swiss cheese model of defense: multiple layers, each with its own gaps, stacked so that the holes in one layer are covered by the next. Card locking, out-of-state blocking, chip cards, terminal blocking, and real-time transaction blocking each address a different dimension of the threat. Together, they can close the gaps that criminals currently exploit.

The EBT system needs another layer. And the technology already exists.

What is real-time transaction blocking?#what-is-real-time-transaction-blocking

In mainstream financial services, real-time transaction blocking (RTTB) is a common practice. When a credit card company detects a suspicious charge, the transaction is stopped before it completes. The cardholder gets an alert. They confirm or deny the charge and on the rare occasion a blocked transaction was actually a legitimate one, the cardholder is prompted to retry the purchase and the transaction is approved.

This same approach can be brought to EBT.

How it works#how-it-works

Every EBT purchase already goes through an authorization flow: a cardholder swipes their card, the retailer’s point-of-sale system sends the transaction to a third-party processor, the third-party processor sends the transaction to the EBT processor, the EBT processor checks the card’s validity and balance, and the transaction is approved or denied.

Real-time transaction blocking adds a small, fast step to this existing flow. Before a transaction is approved, it’s checked against a fraud detection algorithm. If the transaction does not trigger a flag in the fraud detection algorithm (as the vast majority will not) it proceeds with no perceptible difference for the cardholder or the retailer. If the transaction is flagged as highly suspicious, it’s blocked. This additional check adds only milliseconds to the process.

Making RTTB work for EBT#making-rttb-work-for-ebt

Importing a commercial fraud detection tool directly into EBT wouldn’t work because a tool calibrated for mainstream banking patterns would not conform to the unique purchasing patterns and restrictions of the EBT system.

An effective RTTB system for EBT must be designed with several principles in mind.

- The algorithm must be trained on real, national EBT data. The fraud patterns in EBT are distinct. Criminals set up fake payment terminals, clone real retailer identities, and shift liquidation locations constantly. According to internal Propel data informed by user-initiated reports of unrecognized transactions, 70% of retailers that show strong signs of fraud in a given month did not show those signs the month before. Theft networks operate across state lines, creating blind spots in any model trained on data from a subset of states. What's needed is a model informed by actual EBT transaction flows, including data analytics and real reports from cardholders across the country who flag transactions they don't recognize.

- States should have flexibility to set precision levels. A transaction blocking system will need to balance two goals: catching as much theft as possible and avoiding blocking legitimate purchases. A highly precise model will only block transactions that are almost certainly fraudulent, but will miss some theft. A less precise model will catch more fraud, but risks occasionally blocking a legitimate transaction at checkout. States are best positioned to determine the right balance for their populations, and the system should give them that choice with clear data on the tradeoffs.

- The model must update dynamically. Criminals shift tactics, rotate locations, and set up new liquidation points constantly. A static list of known bad actors can't keep pace with that kind of movement. The best way to stay ahead is to continuously incorporate new data. When cardholders report transactions they don't recognize, they become active participants in their own protection. Propel receives tens of thousands of these reports every month, each one a signal that can help the fraud detection model adapt in near real-time to where and how criminals are operating right now. Incorporating inputs that identify new fraud vectors rapidly is an essential building block.

- Blocked transactions must be communicated to cardholders in real time. Any intervention that could block a legitimate transaction should be paired with immediate notification, because the alternative — a family unable to buy groceries at checkout with no explanation — is disruptive and stigmatizing. When a transaction is blocked, the cardholder should receive a notification explaining what happened and provide the ability to confirm or deny the transaction’s authenticity. If legitimate, they can unblock it and retry their purchase within seconds. If not, they're guided through steps to secure their account. This is how credit and debit cards already work, and it's a flow deeply familiar to retailers and consumers alike.

What comes next#what-comes-next

Bringing real-time transaction blocking to EBT requires collaboration among states, EBT processors, and technology partners with deep EBT expertise. It also requires algorithms built specifically for the EBT ecosystem. Propel has built one such model trained on national transaction data informed by tens of thousands of unrecognized transaction reports from EBT cardholders every month. Today, this data powers alerts that help Propel users spot suspicious activity on their accounts. With close state and processor partnerships, it can go further, helping to stop fraudulent transactions before the money ever leaves a cardholder's account.

JPMorganChase has generously awarded $14M in philanthropic investments to help protect Americans from fraud and scams, including funding The Aspen Institute’s work to pilot real-time transaction blocking in EBT with several state agencies. Propel is excited to support these efforts as RTTB moves from concept to practice. These pilots will generate an evidence base for broader rollout, shaped directly by the states that choose to lead the way.

EBT theft is too widespread and too damaging to ignore. Cardholders need multiple layers of protection, and states have the opportunity to deliver it.

For state agencies interested in exploring real-time transaction blocking, reach out at gov@propel.app.